Category creation is the most romantic idea in B2B marketing. Name the problem. Own the vocabulary. Become the Gartner Magic Quadrant leader in a category you defined. The company that names the category writes the rules.

It is also one of the most expensive bets an early-stage company can make, and most of the time it is not the bet the company thinks it is.

HubSpot created Inbound Marketing. That is the example every founder cites. What that example rarely includes: HubSpot was founded in 2006 and spent years building the content engine and the community that made the category real before the term became standard. The category creation happened over a decade, not a quarter. Most Series A companies have 18 to 24 months of runway. Inbound Marketing as a category took longer than that just to get the first Google search volume.

The category creation conversation is the one I push back on hardest in early-stage engagements. Not because the ambition is wrong. Because the timing almost never is.

What category creation actually costs

Category creation requires educating buyers about a new way to think about a problem — which means your budget allocation between brand awareness and demand generation looks very different than a company playing in an established category they already have a frame for. Every piece of content, every sales call, every conference talk has to do double the work: first convince the buyer that the old category no longer fits their problem, then convince them that your product solves the redefined problem better than the alternatives.

That double work has a price. Practitioners who have watched it play out put it plainly: the costs of positioning yourself as the only brand in a new category are astronomical. Making a new market is costly and comes with far more risk, in return for larger payoffs that require capital you may not have.

Category creation is not a positioning strategy. It is a capital allocation decision. The question is not whether your product deserves its own category. It is whether your runway can fund the education required before the category generates its own inbound demand.

Drift tried twice. The first attempt, Conversational Marketing, worked well enough that competitors adopted the term. It worked because the behavior Drift was describing (qualifying leads through chat in real time instead of routing them to forms) was genuinely different enough that buyers could not map it cleanly to an existing category. Even then, one analyst noted years later that conversational marketing never fully became a thing, as buyers eventually concluded forms were more efficient for most use cases.

The second attempt, Revenue Acceleration, failed. David Cancel discussed it as a failure publicly. The category never took hold because it was not describing a new behavior. It was describing an ambition. A positioning rename is not a category. Buyers can feel the difference.

What most founders actually have

When I sit with a founding team that believes they are creating a new category, the conversation almost always arrives at the same place: the product is genuinely better for a specific type of buyer than anything else in the existing category. That is real and worth protecting. But the framing of "we need to create a new category to explain why" is almost always a signal that the ICP definition is not specific enough yet, not that the category is wrong.

A product that is genuinely better for a specific buyer in an existing category does not need buyers to unlearn their current frame. It needs to find the sub-segment of the existing category where the existing vocabulary already fits the product better than it fits anyone else. That is a tractable problem on the budget you have. It does not require a content engine, a multi-year community build, or a category name that nobody is searching for yet.

The sub-segment question has a specific, findable answer. It comes from the closed-won data, from sales call recordings, from asking the five best customers what they had already tried before they found this product. The answer almost always reveals a corner of the existing category that is underserved by the generic leaders, where the product's specific strengths are most visible, and where no direct competitor currently has the same claim.

What sub-segment positioning looks like in practice

The sub-segment position does not require new vocabulary. It requires being more specific than the category leader is willing to be. Category leaders stay broad because they are protecting market share across the whole category. That breadth is their business model and their constraint. A narrower company with a better answer for one type of buyer can own that corner without competing on the category leader's terms.

None of these create a new category. All of them own a specific buyer in an existing category well enough that the buyer who fits recognizes themselves immediately in the description. That recognition is the conversion mechanism. Not education. Not category vocabulary. The buyer sees themselves and knows this is for them.

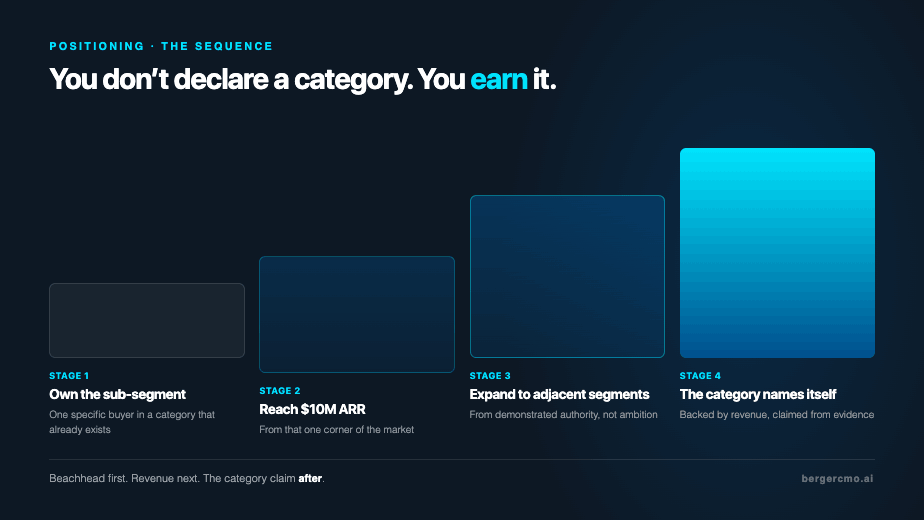

From beachhead to category

The sub-segment approach is not a surrender. It is a sequence. Own the corner first. Get to $10M ARR from the corner. By then, the company has the revenue to fund the category conversation from a position of demonstrated authority rather than a position of ambition. The category claim, if it is still the right one, will be backed by a customer base that proves it. The customers will have language for the problem the product solves. That language is a category emerging from evidence rather than being declared in advance.

Most of the companies that eventually achieved category-defining scale started with a specific sub-segment. They did not start by declaring a new category. They started by being undeniably right for one specific type of buyer, and the category named itself after the revenue came.

The category creation conversation in an early-stage engagement is usually a sign that the positioning work has not been done yet. The founding team has a product that is genuinely differentiated, but has not yet found the specific buyer for whom that differentiation is most visible and most valuable. The instinct is to solve that gap by reframing the entire market. The faster solution is to find the buyer first.

If you are currently describing your product as creating a new category and the pipeline numbers are not where they should be, the question worth asking is whether buyers are finding you by searching for your category name or by stumbling onto you through existing category searches and recognizing something specific. The answer tells you whether the category is working or whether the sub-segment work still needs to happen.

One note on the board conversation: the category creation argument is worth having with investors, just at a different moment. A $10M ARR company telling investors it owns a new category is making a claim backed by evidence. A $2M ARR company telling investors the same thing is making a bet with their capital. The board wants the category story. The sequence that makes it credible is sub-segment first, revenue next, category claim after. That is not retreat. It is the order that makes the category claim land.