It was sometime around 2008 or 2009, and Ben Chestnut was sitting across from a venture capitalist who wanted to give him a lot of money. Email marketing was exploding. Constant Contact had just raised $107 million in its IPO. The market was enormous and getting more enormous by the quarter. Every investor in Silicon Valley knew it.

Chestnut said no.

He had said no before. He would say no again. The VCs wanted Mailchimp to acquire servers and merge with competitors. Smart advice, by any conventional playbook. But Chestnut recognized something the investors did not: accepting their money meant accepting their strategy. And their strategy required a different GTM motion than the one he was building. So he kept saying no. For two more decades. When Intuit acquired Mailchimp in 2021, it paid $12 billion for a company that had never taken a dollar of venture funding.

Most founders read that story as a parable about independence. It is actually a parable about marketing.

What the funding decision is actually deciding

The conventional frame goes like this: bootstrapping is for founders who want control and can grow organically. VC is for founders who need speed or capital to compete. Same business, different amounts of money. The decision is financial.

The evidence says it is not financial. It is structural. And the structure it changes is your go-to-market.

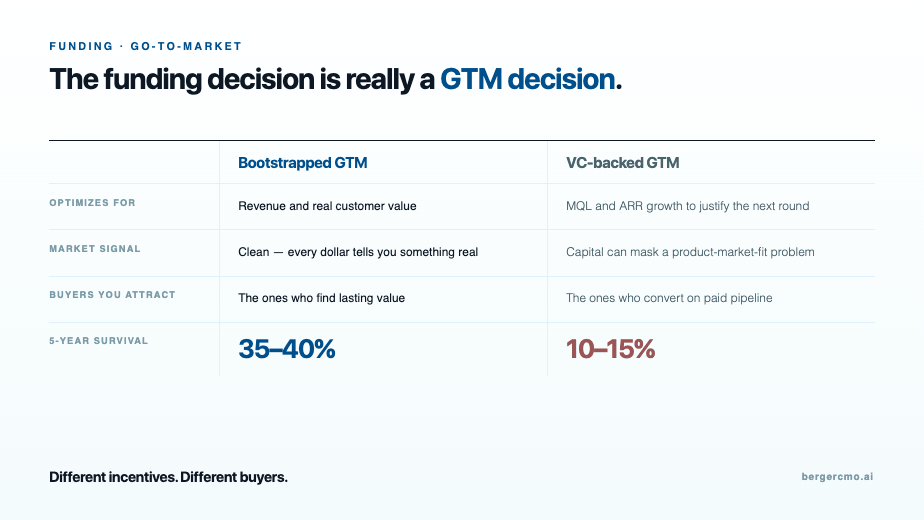

When you take institutional money, you begin optimizing for the metrics your investors need to see. MQL volume. Pipeline coverage. Demo requests. Top-line ARR growth. These are real metrics. But they are downstream of a prior question that often never gets asked: what does your specific buyer actually need to see before they trust you enough to sign?

I use MQL in this post as a stand-in for investor-facing growth metrics, because it is the most common example. But I am not a believer in MQLs as a day-to-day goal for marketing teams. The problem is that the metric shapes the behavior. Goal a marketer on MQLs and they will do what the metric rewards: put forms in front of content, lower the scoring threshold, chase volume over quality. I have seen this produce beautiful-looking dashboards and empty pipelines. The activities I goal marketing on are SALs and SQLs. Real ICP fit. Real intent signal. Someone who asked to speak with us, or who behaved in a way that suggests they are actively looking for a solution. That number is harder to hit. It is also the one that matters.

When you have 18 months of runway and a board pushing for MQL growth, you build marketing that produces MQL growth. When you have three years of runway and a P&L that has to work on its own, you build marketing that produces revenue. Those are different programs. They attract different buyers. They produce different messaging. And only one of them tells you whether you actually have product-market fit before you have spent the capital to find out.

The most dangerous thing about raising too early is not the dilution. It is that you start optimizing for metrics that look like traction but are not the same as demand.

The $550K company that reached $70M ARR

Calendly raised $550,000 in seed funding in April 2014. That was the only outside capital it took for the next seven years. No Series A. No growth round. By the time it raised a $350 million Series B in January 2021, Calendly had $70 million in ARR. The ARR-to-funding multiple at that raise was 109 times.

To understand what made that possible, you have to look at the GTM. Calendly had no dedicated sales team at $4 million ARR. The product spread entirely through use. Someone sent a Calendly link to schedule a meeting. The recipient experienced the product before ever creating an account. They signed up. They sent their own Calendly link. Each calendar invitation was a product demo. The GTM motion was embedded in the product itself, visible only to people who were experiencing a real problem it solved.

That motion is not compatible with investor pressure to hire salespeople the moment enterprise interest appears. It requires patience that VC math does not permit. Calendly could build it because it had no one to answer to except the customers who were paying for the product. The restraint was not a limitation. It was the strategy.

Atlassian ran the same playbook a decade earlier. Started in 2002 on $10,000 on a credit card. Bootstrapped for eight years with 40 consecutive profitable quarters before accepting $60 million in venture capital. Now publicly traded on the NASDAQ. When the funding eventually came, it came on Atlassian's terms, at a valuation that reflected a decade of genuine customer-driven growth. Not investor-facing metrics. Revenue.

What the VC incentive structure does to your GTM

VC funds invest in ten companies expecting seven to fail, two to return capital, and one to return the entire fund. That math requires companies that can 100x or 1000x. A company that grows steadily to $30 million in profitable ARR and stays there is, by almost any normal measure, a success. By the VC return model, it is a write-off.

When you take that money, you adopt that math. Not because your investors are unreasonable. Because the incentive structure is real and the conversations that follow a raise are shaped by it. The board wants to see MQL growth because MQL growth is a leading indicator of the ARR growth that justifies the next round. The next round justifies the fund. The fund needs one company to 100x.

None of that is wrong. It is just a different optimization function than the one that produces Mailchimp or Calendly or Basecamp. And the problem is not that founders take VC from bad investors. The problem is that founders take VC before they know which type of market they are in and what GTM motion their buyers actually respond to.

Raise into a proven GTM and the capital accelerates something real. Raise before the GTM is proven and the capital accelerates your search for product-market fit at a burn rate that may not give you enough time to find it.

How to think about the decision as a GTM question

Bootstrapped startups have a five-year survival rate of 35 to 40 percent. VC-backed companies survive at 10 to 15 percent over the same period. This is not a verdict on which path is better. It is evidence that the incentive structures produce fundamentally different decisions, and that a lot of VC-funded companies are placed on a trajectory that most businesses cannot survive.

The question worth asking before you raise is not "how much do I need?" It is "what GTM motion have I proven works at small scale, and does the capital I am about to take accelerate that motion or replace it?"

Mailchimp's answer, in 2009, was that the VCs wanted to replace his motion. So he walked away. Calendly's answer, for seven years, was that it did not need capital to prove the motion, and raising before that proof would have disrupted the very thing that made the product spread. When both companies finally raised, or chose not to, they did so from a position of evidence rather than hope.

The funding decision is not reversible in the way founders tend to think. You can always raise later. But you cannot easily un-optimize a GTM that was built for investor metrics once the organization has been built around it. The messaging, the channels, the team structure, the KPIs. All of it calcifies around whatever you were measuring in the first 18 months.

Chestnut understood this in 2009 without having the words for it. He was not anti-VC. He was pro-clarity. He knew what his GTM required and he knew that the money came with a strategy attached. He chose the strategy that fit his market over the strategy that fit the investors' return model.

If you have already raised and you recognize the drift happening in real time, the work is not about undoing the raise. It is about identifying which parts of your original GTM motion are still intact, which have been overwritten by investor-facing pressure, and making deliberate decisions about which customer signals you protect going forward. That is a conversation you can have with your board. It is also a conversation worth having before the next planning cycle locks in another year of the wrong metrics.

That is the question. Not bootstrap or VC. What does your GTM require, and which funding structure lets you build it? If you are pre-raise and working through that decision, or post-raise and feeling the drift, the 30-minute call produces one thing: a clear read on which parts of your current GTM are working for your buyers versus which are working for your deck. That is a useful thing to know regardless of what comes next →